Are you thinking about selling your house? If so, today's mortgage rates may make you wonder if that's the right decision. Some homeowners prefer to sell and take on a higher mortgage rate on their next home. If you're worried about this too, know that even though rates are high right now, so is home equity. Here's what you need to know.

Bankrate explains what equity is and how it grows:

"Home equity is the portion of your home you've paid off and own outright. It's the difference between what the home is worth and how much is still owed on your mortgage. As your home's value increases over the long term and you pay down the principal on the mortgage, your equity stake grows."

In other words, equity is how much your home is worth, minus

If you’re planning to buy a home, one thing to consider is what experts project home prices will do in the future and how that might affect your investment. While you may have seen negative news over the past year about home prices, they’re doing far better than expected and are rising across the country. And data shows experts forecast home prices will keep appreciating.

Experts Project Ongoing Appreciation

Pulsenomics polled over 100 economists, investment strategists, and housing market analysts in the latest quarterly Home Price Expectation Survey (HPES). The results show what the panelists project will happen with home prices over the next five years. Here are those expert forecasts saying home prices will go up every year through

One question that’s top of mind if you’re considering moving today is: Why is it so hard to find a house to buy? And while it may be tempting to wait it out until you have more options, that’s probably not the best strategy. Here’s why.

There aren’t enough homes for sale, but that shortage isn’t just a problem today. It’s been a challenge for years. Let’s look at some of the long-term and short-term factors that have contributed to this limited supply.

Underbuilding Is a Long-Standing Problem

One of the big reasons inventory is low is because builders haven’t been building enough homes in recent years. The graph below shows new construction for single-family homes over the past five decades, including the long-term average for housing

If you hope to buy a home this year, you’re probably paying close attention to mortgage rates. Since mortgage rates impact what you can afford when you take out a home loan – and affordability is a challenge today – it’s a good time to look at the big picture of where mortgage rates have been historically compared to where they are now. Beyond that, it’s essential to understand their relationship with inflation for insights into where mortgage rates might go soon.

Giving Context to the Sticker Shock

Freddie Mac has been tracking the 30-year fixed mortgage rate since April 1971. Every week, they release the results of their Primary Mortgage Market Survey, which averages mortgage application data from lenders across the country (see graph

Toward the end of last year, there were several headlines saying home prices would fall substantially in 2023. That led to a lot of fear and questions about whether there would be a repeat of the housing crash that happened back in 2008. But the headlines got it wrong.

While there was a slight home price correction after the sky-high price appreciation during the ‘unicorn’ years, home prices didn’t come crashing down nationally. If anything, prices were a lot more resilient than many people expected. Let’s look at some of the expert forecasts from late last year stacked against their most recent forecasts to show that even the experts recognize they were overly pessimistic.

Expert Home Price Forecasts: Then and Now This visual shows the

Even though activity in the housing market has slowed from the frenzy that was the ‘unicorn’ years, it’s still a seller’s market because the supply of homes for sale is so low. But what does that mean for you? And why are conditions today so good if you want to sell your house?

The latest Existing Home Sales Report from the National Association of Realtors (NAR) shows housing supply is still astonishingly low. The number of available homes on the market measures housing inventory. It’s also measured by months’ supply, meaning the number of months it would take to sell all those available homes based on current demand. In a balanced market, there’s usually about a six-month supply. Today, we have only about three months’ supply of homesat the

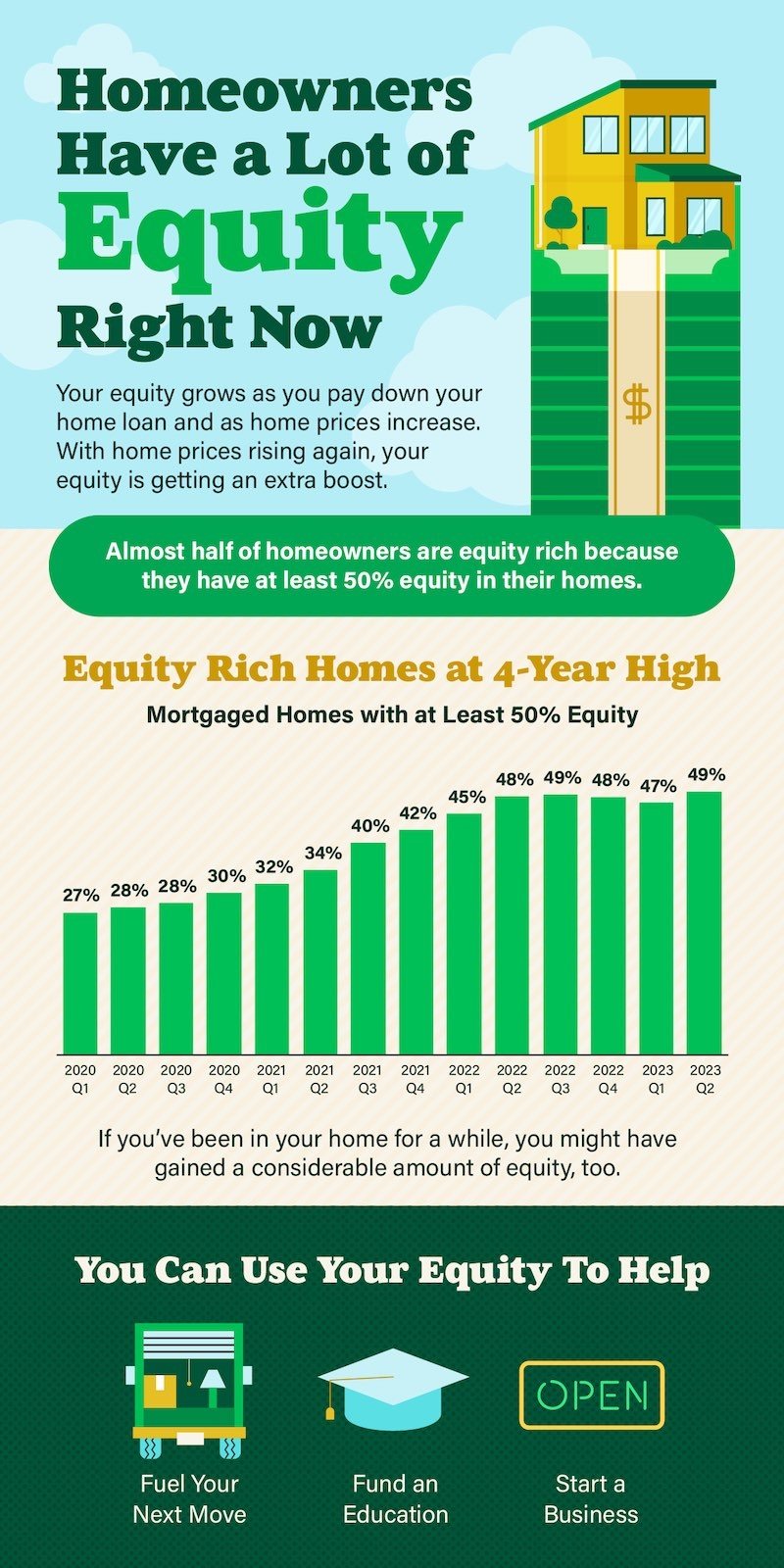

Your equity grows as you pay down your home loan and prices increase. With home prices rising again, your equity is getting an extra boost.

Almost half of homeowners are equity-rich because they have at least 50% equity. If you’ve been in your home for a while, you might have also gained a considerable amount of equity.

Want to find out how much equity you have? Contact The Aaronson Group. Call 949-388-5194 Email: info@previewochomes.com

Have you ever wondered how inflation impacts the housing market? Believe it or not, they’re connected. Whenever there are changes to one, both are affected. Here’s a high-level overview of the connection between the two.

The Relationship Between Housing Inflation and Overall Inflation

Shelter inflation is the measure of price growth specific to housing. It comes from a survey of renters and homeowners by the Bureau of Labor Statistics (BLS). The survey asks renters how much they’re paying in rent and homeowners how much they’d rent their homes for if they weren’t living in them. Much like overall inflation measures the cost of everyday items, shelter inflation measures the cost of housing. And for four consecutive months, based on that

Even though you may feel reluctant to sell your house because you don't want to take on a higher mortgage rate than the one you have now, there's more to consider. While the financial side of things does matter, your personal needs may matter just as much. As an article from Bankrate says:

"Deciding whether it's the right time to sell your home is a personal decision. There are numerous important questions to consider, both financial and lifestyle-based, before putting your home on the market."

So, ask yourself this: Why did I want to move in the first place?

Your primary motivation wasn't just financial. Why you're thinking about selling has more to do with something changing in your life or a shift in what you need out of your

.png)

.png)

.png)